Featured

Table of Contents

Trustees can be member of the family, trusted people, or banks, depending on your choices and the complexity of the trust. Ultimately, you'll require to. Assets can consist of cash, property, supplies, or bonds. The goal is to ensure that the trust is well-funded to meet the child's lasting financial needs.

The role of a in a youngster assistance depend on can not be underrated. The trustee is the private or company in charge of handling the depend on's properties and making sure that funds are dispersed according to the regards to the depend on arrangement. This consists of making certain that funds are used entirely for the child's advantage whether that's for education, treatment, or everyday expenses.

They need to also offer routine records to the court, the custodial parent, or both, relying on the regards to the depend on. This responsibility ensures that the trust is being managed in a method that advantages the kid, protecting against misuse of the funds. The trustee likewise has a fiduciary task, meaning they are legally obliged to act in the very best rate of interest of the child.

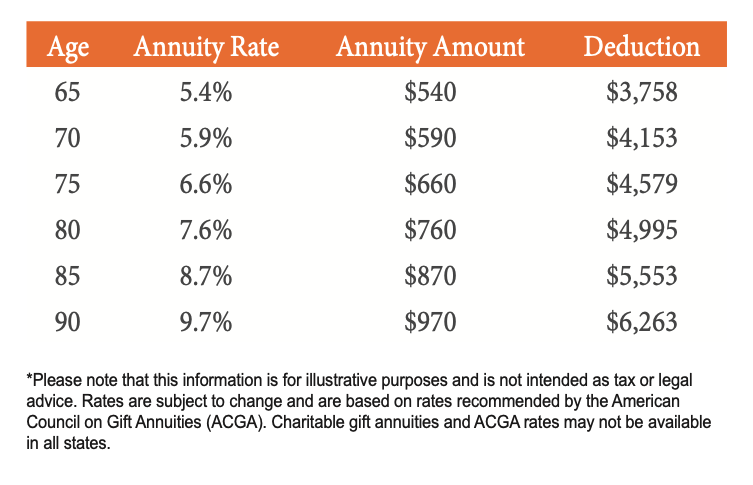

By buying an annuity, moms and dads can ensure that a taken care of quantity is paid frequently, no matter of any type of fluctuations in their revenue. This provides satisfaction, understanding that the kid's demands will certainly remain to be satisfied, no matter the economic conditions. One of the crucial advantages of utilizing annuities for youngster support is that they can bypass the probate process.

Are Annuity Accumulation Phase a safe investment?

Annuities can additionally use protection from market fluctuations, making certain that the youngster's financial assistance remains steady even in unstable financial conditions. Annuities for Kid Support: A Structured Service When establishing up, it's necessary to think about the tax obligation implications for both the paying parent and the kid. Depends on, depending upon their framework, can have various tax obligation treatments.

In other situations, the beneficiary the youngster might be accountable for paying tax obligations on any type of circulations they obtain. can likewise have tax ramifications. While annuities provide a steady income stream, it's important to understand exactly how that revenue will be exhausted. Depending upon the framework of the annuity, settlements to the custodial moms and dad or youngster might be taken into consideration gross income.

Among one of the most substantial advantages of using is the capacity to safeguard a kid's economic future. Depends on, specifically, use a level of security from lenders and can make sure that funds are made use of sensibly. A count on can be structured to guarantee that funds are just made use of for specific functions, such as education and learning or medical care, avoiding abuse.

How do I get started with an Annuity Interest Rates?

No, a Texas kid assistance trust is particularly designed to cover the kid's essential demands, such as education, healthcare, and daily living expenses. The trustee is lawfully bound to guarantee that the funds are made use of only for the advantage of the kid as outlined in the depend on contract. An annuity provides structured, foreseeable payments gradually, guaranteeing consistent financial backing for the kid.

Yes, both child assistance trust funds and annuities come with potential tax obligation effects. Trust fund income may be taxable, and annuity settlements might likewise be subject to tax obligations, depending on their framework. Given that many senior citizens have been able to save up a nest egg for their retired life years, they are commonly targeted with fraudulence in a method that younger people with no cost savings are not.

In this atmosphere, consumers should equip themselves with information to secure their interests. The Attorney general of the United States gives the complying with tips to consider prior to buying an annuity: Annuities are complex financial investments. Some bear facility high qualities of both insurance coverage and safeties products. Annuities can be structured as variable annuities, fixed annuities, immediate annuities, delayed annuities, etc.

Consumers ought to read and comprehend the syllabus, and the volatility of each investment listed in the program. Investors ought to ask their broker to discuss all conditions in the prospectus, and ask inquiries about anything they do not understand. Dealt with annuity products may also carry dangers, such as long-lasting deferment periods, disallowing financiers from accessing all of their money.

The Attorney General has filed legal actions versus insurance coverage firms that offered unsuitable deferred annuities with over 15 year deferral periods to financiers not expected to live that long, or that require accessibility to their cash for wellness care or helped living costs (Annuity withdrawal options). Investors need to make certain they recognize the long-term repercussions of any kind of annuity acquisition

What are the tax implications of an Tax-efficient Annuities?

The most considerable fee associated with annuities is usually the abandonment charge. This is the percent that a customer is billed if he or she takes out funds early.

Customers may wish to seek advice from a tax specialist before purchasing an annuity. The "security" of the investment depends on the annuity. Be careful of representatives who aggressively market annuities as being as risk-free as or far better than CDs. The SEC alerts consumers that some sellers of annuities products urge consumers to switch to an additional annuity, a method called "spinning." Agents may not appropriately disclose fees linked with switching investments, such as new surrender charges (which generally start over from the date the item is switched), or considerably modified benefits.

Representatives and insurance policy firms might use bonus offers to tempt financiers, such as additional interest points on their return. Some dishonest representatives motivate consumers to make unrealistic investments they can't afford, or acquire a long-lasting deferred annuity, also though they will certainly require accessibility to their money for wellness care or living expenditures.

This area provides details valuable to senior citizens and their family members. There are several events that may impact your benefits. Provides information frequently asked for by new retirees consisting of transforming wellness and life insurance alternatives, COLAs, annuity payments, and taxable parts of annuity. Explains just how benefits are influenced by occasions such as marital relationship, separation, fatality of a partner, re-employment in Federal service, or inability to manage one's funds.

Are Fixed Annuities a safe investment?

Key Takeaways The recipient of an annuity is a person or organization the annuity's owner designates to get the agreement's survivor benefit. Different annuities pay to recipients in different ways. Some annuities might pay the beneficiary constant repayments after the agreement holder's fatality, while various other annuities might pay a fatality advantage as a lump sum.

{kind=link}

Table of Contents

Latest Posts

Highlighting the Key Features of Long-Term Investments A Comprehensive Guide to Pros And Cons Of Fixed Annuity And Variable Annuity Defining Annuities Variable Vs Fixed Pros and Cons of Various Financ

Exploring the Basics of Retirement Options Key Insights on Your Financial Future What Is the Best Retirement Option? Advantages and Disadvantages of Fixed Annuity Vs Equity-linked Variable Annuity Why

Breaking Down Your Investment Choices Key Insights on Fixed Indexed Annuity Vs Market-variable Annuity What Is Immediate Fixed Annuity Vs Variable Annuity? Advantages and Disadvantages of Different Re

More

Latest Posts